US reaction: CPI provides some reality check

- 11 Septiembre 2024 (5 min read)

KEY POINTS

US CPI August headline inflation rose by 0.2% on the month, in line with expectations, seeing the annual rate fall to 2.5% its slowest pace since February 2021. However, core inflation rose by a faster than expected 0.3% on the month (0.28%), marginally above the expected 0.2%, although the annual rate remained unchanged at 3.2% (unadjusted) as expected.

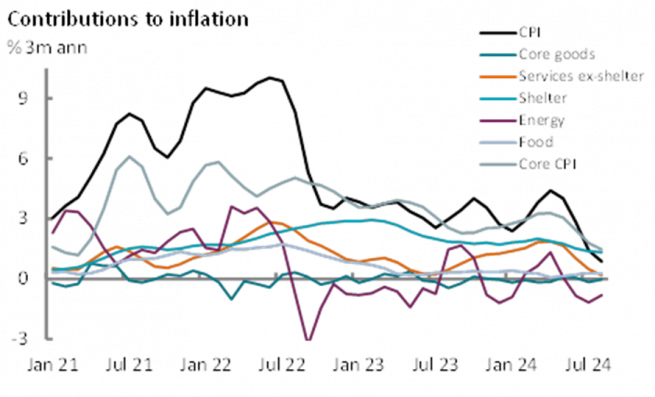

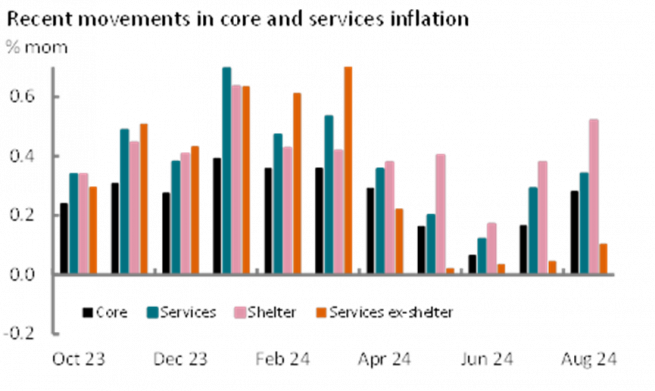

In broad terms, goods price inflation continued to slow, -0.2% on the month and the same as the average pace of decline seen since June 2023. The annual pace of goods decline was -1.2% and its joint lowest since the start of the pandemic. Energy also continued to fall, including through household energy and motor fuel costs. This had the biggest impact on headline inflation compared to the rise in August last year. But overall services inflation accelerated for the second consecutive month to +0.34% having spent two months averaging half that pace in May and June. Services inflation accelerated because of a modest pick-up in ex-shelter inflation (Exhibit 2), which we had considered likely after three months’ of effective stagnation. And a rise in shelter inflation to 0.5% (its highest since the abhorrent January reading), which in turn reflected a rise in owner equivalent rents (OER), which also picked up to 0.5%, its highest since January. By contrast, rents on primary residences settled in at the pace it has averaged since last December. August’s reading is likely to be another erratic spike in OER, with the longer-term typically underpinned by primary rents, which in turn we also expect to ease further. The annual rate of services inflation eased to 4.8% - a 2½ year low.

Exhibit 1 illustrates the two drivers of inflation. Core inflation has softened in trend terms over recent months largely reflecting the softening in ex-shelter services inflation, although the latest reading suggests that this disinflation may be coming to an end. Headline inflation has fallen more sharply thanks to the sharp negative contribution from energy, something that will be exaggerated further in September, but beyond which risks reversing somewhat. In broad terms we remain confident that inflation is coming down and forecast inflation to average 3.0% this year and 2.6% next – consistent with PCE inflation reaching the 2% target sustainably next year. We still expect some deceleration in shelter inflation over the coming quarters and this should offset what we expect to be a less negative contribution from goods and energy inflation in Q4 2024. However, we do not consider inflation to be on track to sustainably undershoot the inflation target. Indeed, we think that the Fed still has a job to do in ensuring a softening in the economy sufficient to achieve a return to target. As such, we consider the scale of Fed cuts currently priced by markets as excessive. We continue to forecast the Fed will start to lower rates by 0.25% next week and continue to see only one further cut this year in December (although acknowledge a risk of a November cut). We do not envisage 100bps of cuts this year as markets. We consider the outlook for next year as election dependent, but stress that a Trump win would likely limit the Fed to two cuts next year if the next administration enacts the demand stimulus and supply restrictive policies Trump suggests.

Market reaction was sharp to today’s 0.03ppt upside beat to core inflation, but to our minds reflected the excessive pricing seen since payrolls, including the acceleration in average earnings to 0.4% on the month in that report. The perceived chances of a 50bp rate cut in September dropped to just over 10% from around 25%, whereas the chances of 125bp of cuts by year-end reduced to just over 10% from 43% before the release. 2-year Treasury yields rose by 7bps to 3.64% - although still a 2-year low; 10-year yields rose 4bps to 3.66% (a 16-month low). The dollar also rose by 0.3% against a basket of currencies, but this is now 1.1% higher than its end-August lows.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.