Summary – Trump-starting the global economy

- 16 Diciembre 2024 (5 min read)

Two major policy uncertainties drive global outlook

Two major policy uncertainties lie at the heart of the global outlook for 2025 and 2026. The first is the extent to which U.S. President-elect Donald Trump translates campaign promises into policy. Our view is that he will not fully deliver what he suggested on tariff increases, migrant deportations, or fiscal loosening. However, we anticipate enough delivery to materially impact U.S. growth as these policies bite into 2026.

The second is how successful China will be in providing stimulus to bolster domestic, particularly household, demand as the economy appears close to a major debt-deflation trap as its property market collapses, impacting local governments and the banking system. Our assumption is of ongoing support, sufficient to deliver a managed deceleration in growth over the coming two years. But these assumptions for the world’s two largest economies will govern the dynamics of the rest of the global economy, as domestic policies adjust to navigate these uncertain, but largely negative, external developments.

Softening U.S. and China growth will dominate

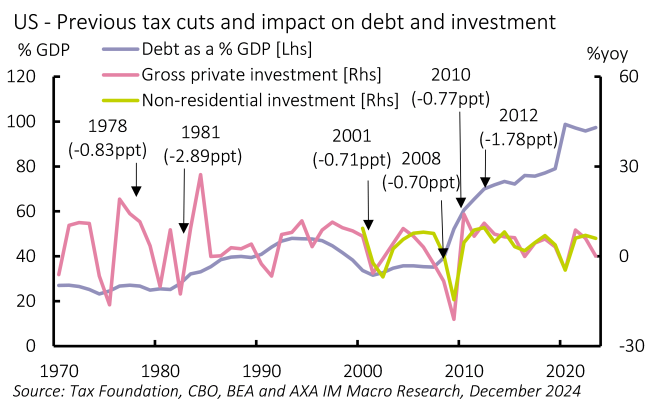

Trump’s re-election has substituted policy uncertainty for political uncertainty. Markets have reacted to this as a growth-positive outcome, but our own assessment is that fiscal measures are likely to be costly while providing little boost (Exhibit 1). Deregulation might provide a noteworthy boost to fossil fuel production but is likely to be less obvious in other sectors, and at best delayed with regards to broader government efficiencies. We also think it is complacent to assume limited implementation of supply shocks, namely immigration and tariff policies. Trump has a mandate to deliver these policies and cabinet picks that include hawkish appointees or those associated with Project 2025 suggest a more focused delivery than during his first term. We forecast solid growth in 2025 at 2.3% (from an expected 2.8% this year) but slowing to a below consensus 1.5% in 2026, while inflation looks set to remain at 3.2% in 2026, reducing the Fed’s space to ease.

Beyond economic policy, we focus on geopolitical risks. The new U.S. administration has suggested a resolution of the Ukraine war, which we interpret as enforced settlement with Russia; a return to “maximum pressure” on Iran, which could impact Middle Eastern alliances; and dialing up trade pressure on China. These threaten to remove key foundations of the current, fragile geopolitical balance and could result in a shift to a new equilibrium. We do not know what such a new equilibrium will look like, but we expect the uncertainty associated with transition to further impact growth.

China has been Trump’s focus with 60% tariffs. Yet China faces its own domestic issues. Its property market crisis, with prices down 15% from the peak in 2021 and 5ppt in 2024 alone, looks set to continue despite recent stimulus. This is weighing on consumer spending, as property represents households’ largest source of investment, and fiscal stimulus/credit creation as China’s entangled local government and regional banking system are also impacted by the property downturn. China faces material challenges to avoid a generation-defining debt-deflation trap. Although we do not expect a full 60% tariff on China, we still foresee an economic impact of around 0.5ppt. We are predicting a range of measures, including further fiscal stimulus and pressure on state-owned enterprises, to boost the household sector in 2025. This should deliver a managed slowdown in China, rather than a severe downturn, and we forecast growth of 4.5% in 2025 (from 4.9% this year) and 4.1% in 2026. However, this depends on delivery of a narrow policy path as the government grapples with unfamiliar headwinds from market forces; risks seem to be skewed to a worse outcome.

Emerging market resilience tested again

Both may have major impacts on the world’s other economies, but no more so than on emerging markets (EMs), particularly those in Asia and Latin America. Many EMs have large exposures to China, and China’s domestic and export producing activities should feed through to raw material and intermediate goods demand. However, where many have been benefiting from the U.S.’s export diversification from China, a new Trump regime may be more focused on associated rising trade surpluses and target additional countries more specifically.

Emerging markets will likely have to adapt policies wisely to manage domestic demand in the face of external headwinds. Monetary policy space remains for further easing, with real rates still elevated in several EMs. However, policies that keep U.S. rates and the dollar higher would reduce the scope for EM easing. Moreover, EM fiscal space remains constricted with primary deficits widening further from pre-pandemic levels in 2024. Policy would be most effective where monetary and fiscal policies work together. EMs should display resilience, but few are likely to lift long-term growth with structural reforms.

Countries with relatively large domestic sectors, including India and Indonesia, look best placed to deliver solid expansion – the latter one of the few with fiscal space to loosen if conditions worsen. Those that have corrected economic imbalances should catch up by 2026, including Turkey, Argentina, and Colombia. South Africa, Egypt, and Nigeria look well placed to benefit from structural reforms. Meanwhile, Brazil’s outlook has seen debt sustainability concerns trigger an unwelcome monetary policy reaction. Mexico may also face difficulties with fiscal austerity at a time when constitutional reforms and U.S. trade protectionism already dampen the outlook.

Europe: Economic stability, political challenges

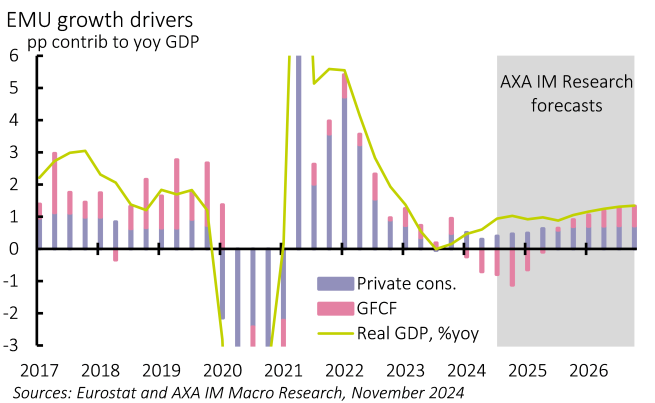

For the Eurozone, recent weakness looks likely to slowly reverse, despite risks posed by the external environment. Inflation’s return to target has lifted real disposable income growth, underpinning an acceleration in consumer spending, despite a marked rise in household saving rates. We predict that this should continue. We are still skeptical of a material recovery in investment (Exhibit 2). However, the evolution of growth headwinds from supply constraints to demand deficiency has increased scope for the ECB to boost activity. It has cut rates, and we see this continuing to 1.5% by end-2025. This should bolster growth, which we forecast to rise to 1.0% in 2025 (from 0.8%) and 1.3% in 2026 as investment begins to respond to lower rates. This outlook remains vulnerable to a more broad-based trade war.

However, weak governments pose a potential risk. In Germany, elections will be held in February instead of September. But even the probable return of a grand coalition looks unlikely to deliver a major turn in fiscal policy, despite the substantial need for long-term investment. France may suffer further political uncertainty with its government likely to face fresh challenges next year. Weak governments are likely to result in slippage from the relatively sharp fiscal tightening planned for next year. They will hamper the EU response to any U.S. tariffs and would impede reaction to any geopolitical developments involving Ukraine or beyond.

We are anticipating that the UK should be politically more stable and credible than in recent years. We forecast a pick-up in growth to 1.5% in 2025 (from 0.9%) and 1.4% in 2026. This should reflect ongoing household real disposable income growth and a loosening in fiscal policy next year, although the latter will fade in 2026. After a brave budget, the UK’s public finances again risk deteriorating if growth fails to match bold expectations, likely requiring further tax increases, spending cuts, and/or borrowing increases. Political stability may begin to attract foreign capital, an effect suggested by the currency this year. But as an open economy, the UK shares the risks of wider Europe from a broader trade war and geopolitical developments.

The global economic outlook is thus poised on the uncertain prospect of policy developments in Washington and Beijing. Our forecasts suggest overall global growth should remain at 3.2% in 2025 but softening to 2.8% in 2026. Next year, excluding China, global growth could be on a par with the post-global financial crisis (2012-2019) pace of activity, although this looks set to slow in 2026 with a more material slowdown in the U.S. and some broader softening through EM. Yet there is a risk that this slowdown reflects renewed structural adjustment which are notably from U.S. supply adjustments meaning, at least for the forecast horizon, relatively muted scope for policy easing and the prospect for relatively elevated term rates.

Source: All data from AXA IM, as of November 2024 unless otherwise indicated.

Disclaimer

Risk Warning

Investment involves risk including the loss of capital.

The information has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. This analysis and conclusions are the expression of an opinion, based on available data at a specific date. Due to the subjective aspect of these analyses, the effective evolution of the economic variables and values of the financial markets could be significantly different for the projections, forecast, anticipations and hypothesis which are communicated in this material.

Disclaimer

This document is being provided for informational purposes only. The information contained herein is confidential and is intended solely for the person to which it has been delivered. It may not be reproduced or transmitted, in whole or in part, by any means, to third parties without the prior consent of the AXA Investment Managers US, Inc. (the “Adviser”). This communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision. © 2024 AXA Investment Managers. All rights reserved